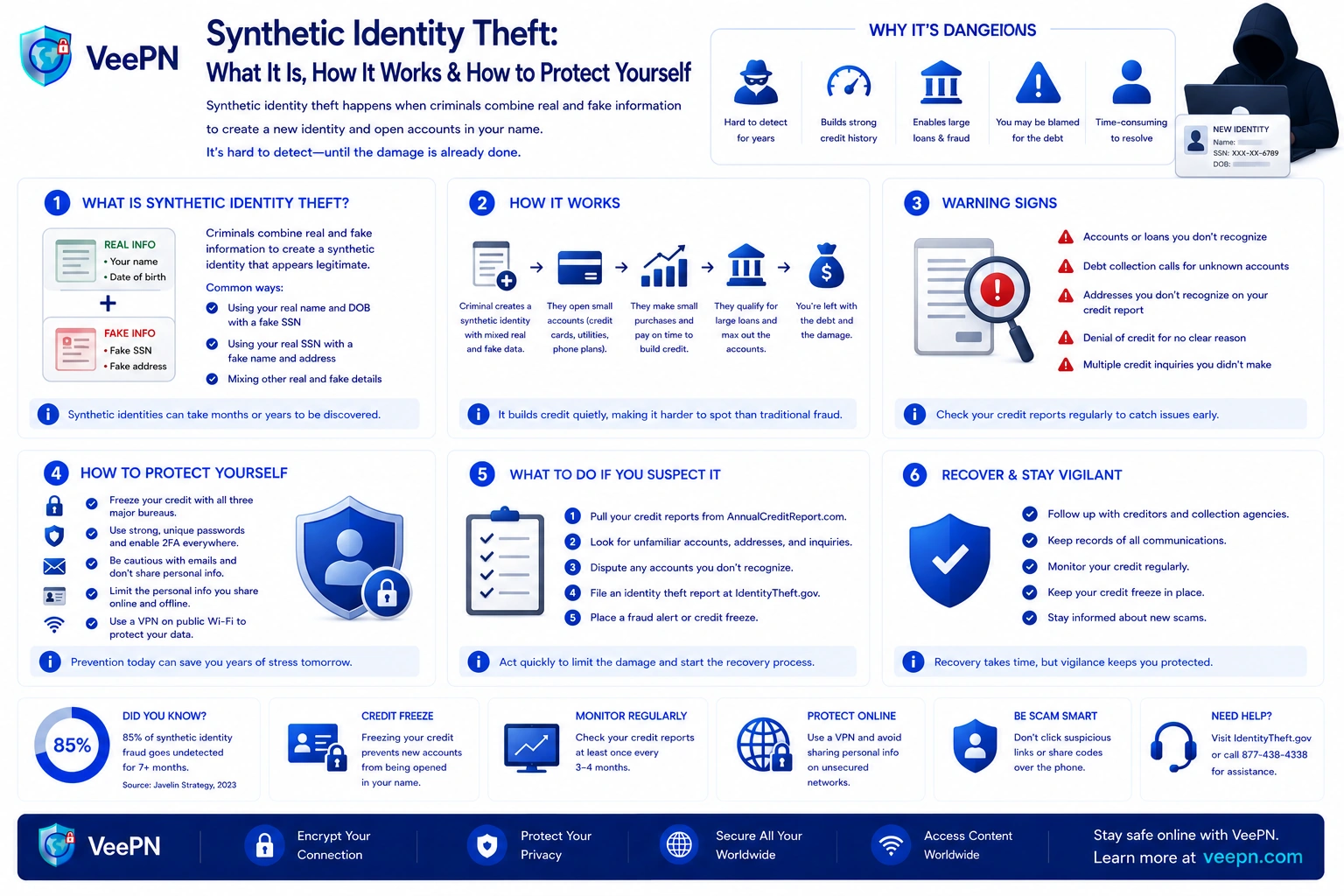

Synthetic Identity Theft: the Fake-person Scam That Can Still Hurt Real People

Most people hear identity theft and imagine a criminal taking over one real person’s life. Synthetic identity theft is different. Here, the fraudster mixes a real piece of data, often a Social Security number, with invented details like a fake name, a new date of birth, or a made-up address to create synthetic identities that look real enough to pass basic checks. That fake profile can then open accounts, build a credit history, and later commit fraud for financial gain.

This is one reason the problem keeps growing. TransUnion said US lenders faced more than $3.3 billion in exposure tied to suspected synthetic identities for the year ending 2024. And in March 2026, American Banker reported that cheap AI toolkits, stolen data, and fake documents were already being used to beat some bank identity verification checks in minutes.

We’ll break down how this scam works, why it is harder to spot than traditional identity theft, the red flags to watch for, and the practical steps that help protect your money, your credit report, and your personal data. We’ll also show where VeePN fits in near the end.

2. Synthetic fraud is not the same as identity theft

3. How a fake identity gets built from real and fake data

4. Identity fraud red flags that may point to a cloned profile

5. Fraud prevention: how to prevent synthetic identity fraud before it grows

6. Why VeePN helps when data breaches feed synthetic identity theft

FAQ

Synthetic identity theft: why synthetic identities are so hard to spot

At first glance, a synthetic profile can look perfectly normal. Real and fake data blended until the new identity reads as legitimate on paper. The SSA inspector general notes that fraudsters often spend months building good credit before making charges and vanishing.

That’s also why the damage stays hidden. With traditional identity theft, a victim usually spots a drained card or frozen account fast. With synthetic fraud there may be no obvious victim at first, so it gets written off as bad debt rather than recognized as identity fraud, buying criminals time to raise credit lines and set up a bigger hit.

Synthetic fraud is not the same as identity theft

The two scams behave differently, and the distinction matters.

- Traditional identity theft hijacks a real person. The criminal uses a stolen identity to charge cards, raid accounts, or access services fast, and the victim usually notices quickly when charges or login alerts appear.

- Synthetic fraud invents a new person on paper. Instead of copying one victim, criminals build fake identities and slowly make them look trustworthy.

- The payout comes later. A fraudster may start with one low-limit account, make small payments to lift the credit score, then go for bigger loans or cards, the “bust-out” pattern.

Because of that, some organizations log this as third-party fraud and others as unpaid credit rather than true fraud. Either way the result is the same: money is lost and trust takes the hit.

How a fake identity gets built from real and fake data

The process isn’t magic. It follows a pattern.

- Collect real data. Criminals gather personal information from data breaches, phishing, hacked accounts, the dark web, and overshared social media.

- Build a believable profile. A real SSN gets paired with a fake name, address, and date of birth, or real details are tweaked just enough to form a new identity. The Social Security Administration documents how these profiles combine real SSNs with false names and birth dates.

- Make it look trustworthy. The synthetic identity opens accounts, becomes an authorized user on a valid card, and builds a clean payment record over time.

- Cash out. Once it has enough trust, the criminal maxes out cards, takes loans, and disappears, which is when the fraud finally becomes visible.

Technology is making this harder to stop. American Banker reported in March 2026 that criminals could buy stolen SSNs, fake documents, AI face generators, and KYC-bypass training for under $300, enough to fool document scans, OCR, and selfie checks that older verification relied on.

Identity fraud red flags that may point to a cloned profile

For regular people the signs look small at first, which is exactly why they matter.

- Unfamiliar accounts or inquiries on your credit report. A card, loan, or hard pull you don’t recognize. The FBI lists unfamiliar charges, new cards, and sudden score drops as common warning signs.

- Bills or debt collection for things you never opened. Strange statements, loan offers, or collection notices can mean someone used your details to build a fake identity.

- Activity tied to a child or older relative who shouldn’t have a credit file. Fraudsters target children, the elderly, and the deceased because those SSNs aren’t watched closely, a child having any credit report at all is a red flag.

- Account-opening attempts you didn’t make. Alerts about new accounts or benefit applications you didn’t start shouldn’t be ignored.

Fraud prevention: how to prevent synthetic identity fraud before it grows

You can’t stop every data leak yourself, but you can make stolen data much harder to use. Start with the basics that actually move the needle.

- Freeze your credit files. If a fraudster can’t easily open new credit in your name, the scam gets much harder to scale.

- Check your credit often, not once a year. The FTC confirms the free weekly-report program through AnnualCreditReport.com is now permanent, making it far easier to catch a strange inquiry or unknown account early.

- Strengthen account security. Unique passwords and two-factor authentication remain basic but important; keep software updated and limit what you share.

- Share less on social media and forms. Oversharing helps thieves guess answers and build believable profiles, the Federal Reserve’s child-fraud guidance warns specifically against this.

- Watch your statements and mailbox. Review cards, loans, and benefits notices; unfamiliar charges and missing mail are classic signs something is off.

For businesses the challenge is bigger: static checks miss too much, so fraud-detection models and cross-channel signals are now essential, but even good models need clean data and real collaboration across lenders to catch synthetic identities at onboarding.

Why VeePN helps when data breaches feed synthetic identity theft

A VPN won’t erase your SSN from a breach or fix a lender’s bad decision. But synthetic fraud runs on leaked data, and VeePN cuts down the easy leaks that feed it.

- Breach Alert. Synthetic profiles are built from data exposed in breaches, Breach Alert warns you when your details surface in known leaks, so you can freeze credit and change passwords before they’re reused.

- NetGuard. Blocks malicious sites, trackers, and shady redirects, the phishing pages that often harvest the personal data behind these profiles.

- AES-256 encryption. On public Wi-Fi, encrypting your traffic makes it harder for anyone to collect login details and personal information in transit.

- No Logs. The privacy tool shouldn’t become another data source, VeePN says it doesn’t store your browsing history, location, or IP.

Want a simple extra layer for protecting your data and cutting exposure on public Wi-Fi? Try VeePN with a 30-day money-back guarantee.

FAQ

The biggest red flags are unfamiliar credit report entries, unexpected cards or bills, debt collection for accounts you never opened, and odd mail for a person who does not really exist. A surprise drop in credit scores or alerts about new account opening attempts can also point to synthetic identity theft. Discover more in this article.

You usually detect it by spotting patterns that do not add up. Check all three credit bureaus, review statements, watch for suspicious activity, and question any notice tied to a fake identity, unknown loan, or strange bank accounts. If a child has a credit file when they should not, that is another strong clue.

Three common forms are financial identity theft, tax fraud, and fraud involving government benefits. The FBI lists false bank or card accounts, false tax filings, and stolen-benefit claims among the common ways criminals misuse personal data.

Look for signs that someone used your real identity to support a new profile: unknown accounts, odd bills, unfamiliar phone calls, missing mail, or new inquiries you did not request. If you suspect your details were used to clone or support synthetic identities, place a freeze, check your reports, and file a recovery plan through IdentityTheft.gov. Discover more in this article.

VeePN is freedom

Download VeePN Client for All Platforms

Enjoy a smooth VPN experience anywhere, anytime. No matter the device you have — phone or laptop, tablet or router — VeePN’s next-gen data protection and ultra-fast speeds will cover all of them.

Download for PC Download for Mac IOS and Android App

IOS and Android App

Want secure browsing while reading this?

See the difference for yourself - Try VeePN PRO for 3-days for $1, no risk, no pressure.

Start My $1 TrialThen VeePN PRO 1-year plan