Is Klarna Safe? Risks, Fees, and Smarter Use

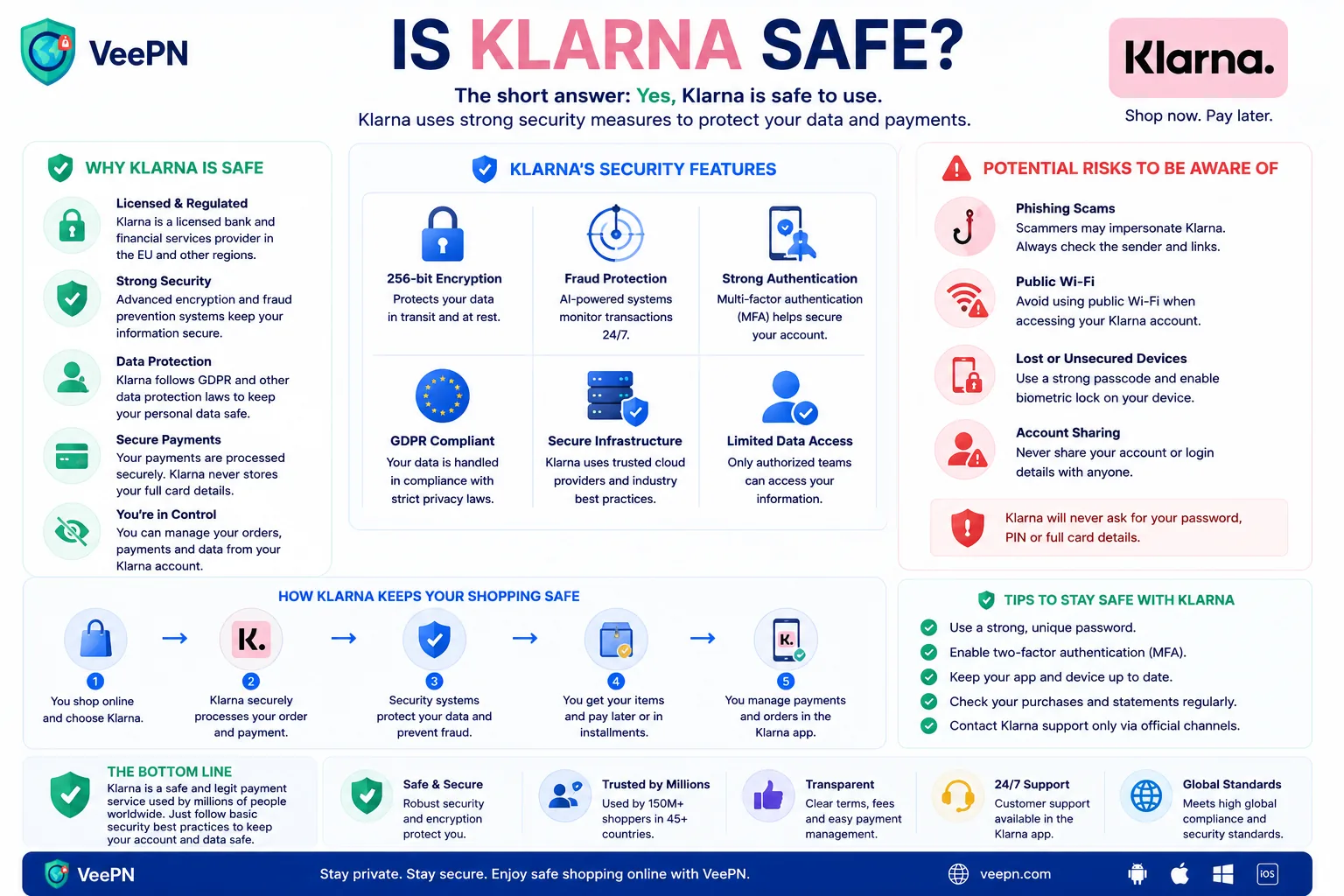

Yes, Klarna is generally safe for most people. It is a real payment company with real safeguards, and millions of people use it for online shopping every month. But the platform being safe does not automatically mean every Klarna purchase is a smart one. The bigger risk is usually not the app itself. It is overspending, weak account security, or falling for scams.

2. Safety vs Financial Risk

3. How To Use Klarna Safely

4. Scam Signs

5. Where VeePN Fits

6. The Two Questions People Mix Together

7. How To Decide Whether Klarna Makes Sense for a Purchase

8. Security Habits for Klarna Users

9. Klarna Scam Patterns

10. Merchant Risk Still Matters

11. BNPL and Credit: Avoid Universal Claims

12. A Safer Klarna Rule of Thumb

13. Privacy Details Shoppers Forget

14. What Safe Use Looks Like

15. The safe-use rule

FAQ

Klarna is a legitimate payment company, and it is generally safe for normal online shopping. The bigger risk is not usually Klarna’s technology. It is overspending, missed payments, account takeover, and fake Klarna messages.

Use Klarna like credit, not like a discount.

What Klarna Does

Klarna offers buy now, pay later options such as splitting a purchase into installments, paying after delivery, or using longer financing where available. The exact products, fees, credit checks, and reporting rules vary by country and product.

That variation matters. Advice for one market may not apply everywhere.

Safety vs Financial Risk

| Question | Short answer | What to check |

|---|---|---|

| Is Klarna a real company? | Yes | Use the official app or checkout |

| Are payments protected? | Generally yes | Merchant terms and Klarna buyer policies |

| Can late fees apply? | Yes, depending on product and market | Payment schedule before confirming |

| Can it affect credit? | Sometimes | Local Klarna terms and credit reporting |

| Can scammers impersonate Klarna? | Yes | Sender, URL, app notifications |

“Safe” has two meanings here: technical safety and money safety. Both matter.

How To Use Klarna Safely

Only use Klarna for purchases you could afford today. Track payment dates in your calendar. Keep the Klarna app updated. Use a strong password and MFA if available. Do not click urgent payment links from texts or emails. Open the app directly instead.

For expensive items, compare Klarna with a credit card, debit card, or saving and paying in full. Installments can be convenient, but they also make spending feel smaller than it is.

Scam Signs

Be careful with messages saying your Klarna payment failed, your account will be locked, or you need to verify identity immediately. Check the sender and URL. If in doubt, do not tap the link. Open Klarna directly.

Also watch fake stores that offer Klarna logos or checkout language but route you to a fraudulent page.

Where VeePN Fits

VeePN cannot make a bad purchase affordable or guarantee a merchant is honest. It can help with the privacy and security around online shopping.

The VPN protects traffic on public Wi-Fi while you browse or pay. Data Breach Alert can warn if an email tied to shopping or payment accounts appears in known breaches. Alternative ID can help keep your primary email away from low-trust stores and newsletters. VeePN Antivirus can help on supported devices if a fake store or malicious ad tries to push unsafe downloads.

The Two Questions People Mix Together

“Is Klarna safe?” usually means two different things.

The first question is security: does Klarna protect accounts, payments, and personal information? Klarna publishes security guidance for users and offers account-protection features such as app login controls and fraud monitoring. Users still need to avoid fake messages and protect the email account connected to Klarna.

The second question is financial behavior: can buy now, pay later make spending harder to control? Yes. That risk exists even if the app works exactly as designed.

| Risk area | Klarna can help with | User still controls |

|---|---|---|

| Payment processing | Secure checkout and fraud checks | Choosing trusted merchants |

| Account access | Login protections | Password, MFA, email security |

| Purchase disputes | Support processes | Keeping receipts and evidence |

| Payment schedule | Reminders and app visibility | Not stacking too many plans |

| Credit impact | Product disclosures | Reading local terms before checkout |

| Phishing | Security reporting channels | Avoiding links in texts and emails |

That split matters. Do not treat a budgeting problem as a cybersecurity problem, and do not treat phishing as a budgeting problem.

How To Decide Whether Klarna Makes Sense for a Purchase

Before using Klarna, ask four questions:

- Would I buy this at full price today?

- Do I know the total repayment dates?

- Do I have enough money for every installment without assuming future income?

- Is the merchant trustworthy without Klarna?

If the answer to any of those is no, Klarna may make the purchase feel safer than it is. Buy now, pay later works best for planned purchases, not emotional purchases.

The U.S. Consumer Financial Protection Bureau has published consumer resources on buy now, pay later because these products can create confusion around multiple payment plans, fees, disputes, and credit reporting. The details vary by market, so check the terms shown in your own checkout flow.

Security Habits for Klarna Users

Use the official Klarna app or website. Do not update payment details through an email or text link. Keep the phone locked with biometrics or a strong passcode. Protect the email account connected to Klarna because password resets often depend on email access.

Review Klarna app notifications and payment dates. If a charge appears that you do not recognize, act quickly through the official app or Klarna support. Do not call phone numbers from suspicious messages.

For password safety, the most important account may be your email, not Klarna itself. If an attacker controls your inbox, they may intercept alerts, reset accounts, or hide messages.

Klarna Scam Patterns

Scammers use Klarna because it is a familiar payment name. Common lures include failed-payment texts, fake refund forms, account-lock warnings, fake stores that claim to accept Klarna, and customer-support impersonation.

A safer response pattern:

- Do not tap the link.

- Open the Klarna app yourself.

- Check payment status inside the app.

- Contact the merchant through its official site.

- Report suspicious messages through Klarna’s official support channels.

VeePN’s guide to phishing sites and Link Checker fit here because the risk is not only Klarna. It is the fake page that borrows Klarna’s name.

Merchant Risk Still Matters

Klarna can be part of checkout, but it does not automatically make every store good. A fake shop can still advertise popular payment options. A real shop can still have poor shipping, bad returns, or misleading product pages.

Before using Klarna with an unfamiliar merchant, check the domain age if something feels off, look for a real returns policy, search independent reviews, and avoid deals that are wildly below market price. If the store only exists through ads and has no reputation outside its own site, pause.

For expensive purchases, compare Klarna with a credit card. In some markets, credit cards may provide stronger chargeback or purchase-protection paths. Klarna’s protections depend on product, country, merchant, and terms.

BNPL and Credit: Avoid Universal Claims

Klarna products differ by country. Some involve soft checks. Some financing products may involve credit checks or reporting. Some short-term plans may have no interest if paid on time. Other longer financing can cost more.

Avoid blanket assumptions such as “Klarna never affects credit” or “Klarna is always interest-free.” The accurate move is to read the checkout terms for the exact product and country.

If users already struggle with payment dates, BNPL may not be the right tool. A calendar reminder helps, but it does not fix overextension.

A Safer Klarna Rule of Thumb

Use Klarna when it improves convenience, not when it makes an unaffordable purchase feel possible. If you would be stressed paying the full amount today, splitting it into payments may only delay the stress.

A simple household rule works well: keep a list of all active BNPL plans in one place. Include merchant, amount, due dates, and payment method. The app will show Klarna plans, but it will not show every other installment product, credit card balance, or subscription competing for the same money.

For teens, students, and first-time credit users, this section should be especially direct. BNPL can teach payment discipline when used carefully. It can also normalize buying first and checking affordability later.

Privacy Details Shoppers Forget

Even when a payment app is secure, the purchase creates a data trail: merchant, item category, delivery address, email, phone number, device, and payment schedule. That is normal for online shopping, but it is worth remembering if the purchase is sensitive.

Use a separate shopping email if you want fewer marketing emails tied to your primary inbox. That is where Alternative ID can fit naturally. It does not change Klarna’s repayment terms, but it can reduce unnecessary exposure of your main email address.

What Safe Use Looks Like

Safe use looks ordinary: buy from a merchant you trust, read the payment schedule, set reminders, keep the app updated, ignore payment links in texts, and open Klarna directly when something looks wrong. If the purchase is expensive or the terms are unclear, pause before confirming.

That practical description is more useful than a broad yes-or-no answer.

Respect the reader’s intelligence: Klarna can be safe as a payment tool and still be a poor choice for a specific purchase. Both things can be true at the same time.

The safe-use rule

Klarna is generally safe as a payment platform, but it can still be risky for your budget if you stack purchases or miss payment dates. Treat it like scheduled debt, not a discount. For security, use the official app, ignore urgent payment links, and protect the email account tied to Klarna.

The checkout terms are the source of truth because Klarna products, fees, financing, and credit handling vary by country and purchase type.

If the terms feel unclear at checkout, pause. A payment plan should make the schedule easier to manage, not harder to understand.

FAQ

Is Klarna safe to give personal information to?

Use Klarna only through the official app, website, or trusted merchant checkout. Do not share personal data through email links, text messages, or phone calls claiming to be support.

What are the downsides of Klarna?

The main downsides are overspending, missed payments, possible fees, and confusion from having multiple installment plans active at once.

Can Klarna affect credit?

It can, depending on the country and product. Read the terms shown at checkout before accepting financing.

VeePN is freedom

Download VeePN Client for All Platforms

Enjoy a smooth VPN experience anywhere, anytime. No matter the device you have — phone or laptop, tablet or router — VeePN’s next-gen data protection and ultra-fast speeds will cover all of them.

Download for PC Download for Mac IOS and Android App

IOS and Android App

Want secure browsing while reading this?

See the difference for yourself - Try VeePN PRO for 3-days for $1, no risk, no pressure.

Start My $1 TrialThen VeePN PRO 1-year plan